Welcome, adventurer.

We know you’ve been moving strategically through DeFi...

Looking for the best and the most sustainable yields...

We know that your journey has been hard. The volatile market conditions don’t make things easy. You see the highs in APYs, and then you see the drops.

But we are here to help.

For any degen, the first step to conquering DeFi is finding reliable, sustainable sources of yield. And today, we begin that hunt.

Let’s all together explore the vast labyrinth that is DeFi - from the lending protocols to AMMs (automated market makers) to yield aggregators and more...we’ll explore it all and break down for you how they generate their yield and whether they are sustainable.

Ready to begin the journey? Let’s go!

Generating yields from lending pools

Lend your assets to us and generate interest-based on the users who borrow funds from our pool!

Our first stop are the lending pools. The famous DeFi protocols that were all the rage in the summer of 2020. Lending pools are considered a simpler go-to for generating yields in DeFi. Lend your idle cryptoassets to the pool. Users who borrow from these lending pools end up paying an interest rate that you, then, get on your deposited capital. In addition to this, you also get governance tokens for participating in the protocol that also increase in value.

But are the yields that you generate from these protocols sustainable? To answer that, we first need to understand how the yield is generated. A formula, known as the utilization ratio, plays a crucial role here. It is representative of how the pool’s capital is being utilized.

U = Borrows / (Cash + Borrows)

Here, U is the ratio of the total amount of capital borrowed (Borrows) to the total deposited capital (Cash + Borrows). A dynamically changing interest rate helps keep the pool balanced so that

a) it never runs out of funds so borrowers can always take out loans, and/or

b) lenders are able to withdraw their capital if they need to (they wouldn’t be able to do it if all funds have been loaned out).

An ideal scenario would be when there are enough funds within the pool such that lenders keep depositing their capital to the pool and borrowers keep borrowing their capital from the pool. But this is not often the case as the volatility of the market often influences how borrowers/lenders interact with the pool. Let’s understand this through two scenarios.

Scenario 1: An uptrending market

Assume that there is a lot of activity in the market and users are constantly borrowing funds. The pool is gradually shrinking as people are taking away the capital. In this case, the utilization ratio is skewed to the upper side and the interest rate is increased to disincentive borrowing and incentivize lending.

Scenario 2: A downtrending market

Now assume that market is slowly cooling off and lesser number of users are now participating in borrowing from the pools. This means the ratio is skewed to the lower side and the interest rate must be lowered to incentivize incentivize borrowing and disincentivize lending.

These two scenarios show us that the interest rate factors in the prevailing market conditions and is dynamically adjusted to best suit the demand and supply. In a highly volatile market such as crypto, this greatly impacts the sustainability of the yields.

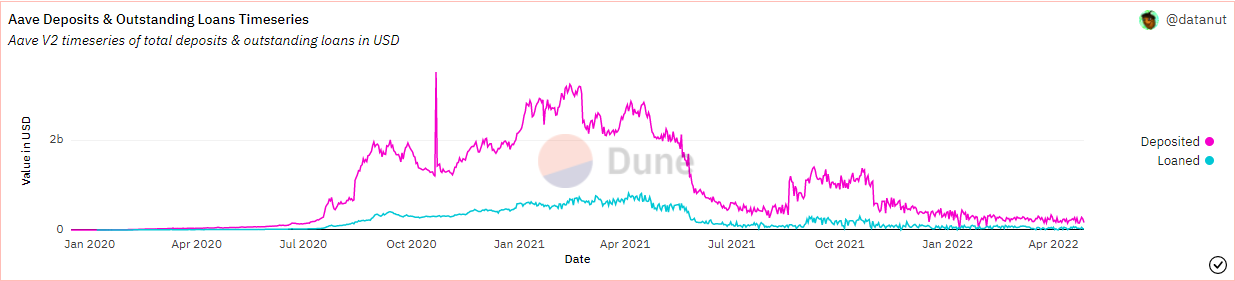

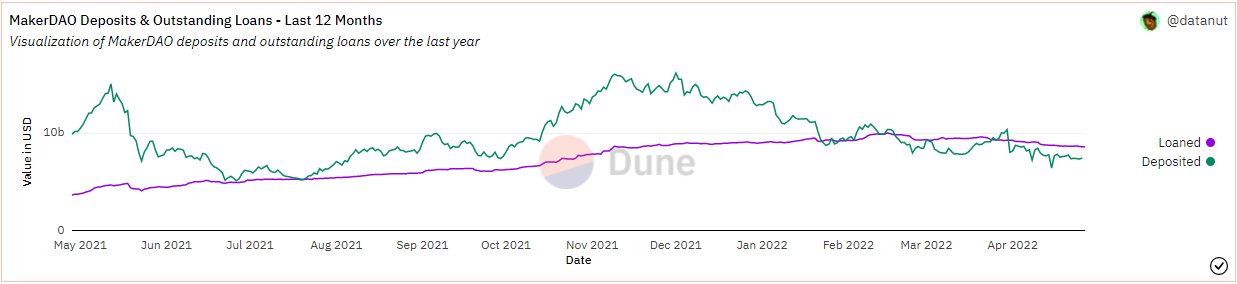

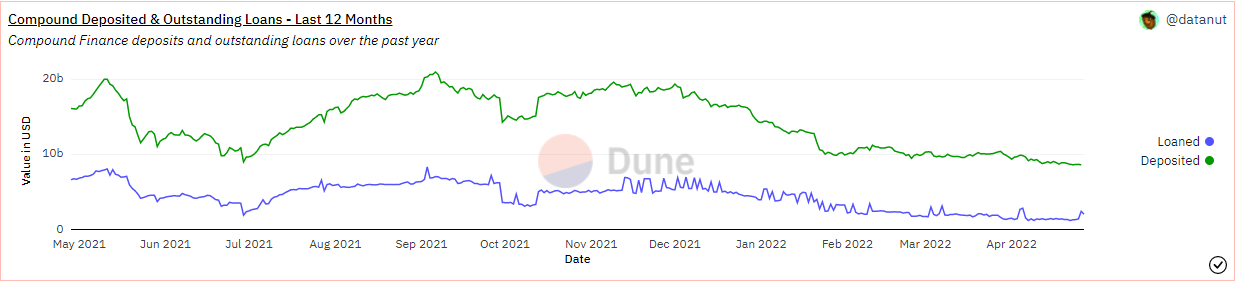

For the interest rate to be lucrative enough for lenders to deposit their capital, the utilization ratio needs to be consistently high (i.e., skewed towards the upper side). If we look at historical data of borrowing on leading lending protocols like Aave, Compound, and MakerDAO, we find that the ratio has been enormously skewed to the bottom as the deposited capital has been greater than the borrowed capital. Here is what the trend has been for the past 12 months on each of these protocols (source).

All of this shows that the interest rate is consistently skewed towards the lower end for the lender, and even in the case of high market activity, it doesn’t change much. Even as of writing, the utilization ratio of Aave and Compound is 0.3 and 0.26 respectively with an average of 1.6% and 1.02% APY across leading assets.

But wait...if the interest on lending on these protocols is low, what makes them still an attractive source of generating yield? The answer lies in how they acquire their users - governance subsidies. Let’s understand.

A simple question that any lending protocol asks is, what can we offer them so they are incentivized to lend to our protocol? They can offer additional subsidies to the users in governance tokens. These tokens help solve two purposes.

- They let us participate in on-chain decision-making for the protocol. We can lock these tokens and send our vote.

- They accrue rewards either from a part of the profit that the protocol generates or from the protocol keeping aside some tokens especially for rewards.

The accrued rewards are, thus, subject to both the supply of these tokens and the protocol's performance. Since they can be freely traded in the market, users can easily dump their share to take their profits and withdraw their invested capital. Any profit-seeking user is then more incentivized:

- to take profits from Protocol A that is offering higher subsidies,

- cash in their profits by dumping the tokens in the market, and

- move to Protocol B to repeat the same process.

This renders the rewards from these governance subsidies unsustainable and further expose them to the volatility within the market.

While lending pools are very secure and the top three on Ethereum collectively hold $31B+ in TVL, lending isn’t a sustainable solution enough for hedging against the highly volatile crypto market. And this puts us back on our journey - to find the most sustainable yields within DeFi.

We must continue our hunt in DeFi...

Can you guess what our next stop would be?